Managing bank accounts, credit cards, investments, and other financial products has become a lot easier over the past few decades, with online service becoming the norm. The next big step, which many financial services companies have already taken, is a good mobile app — but standards for those are getting higher.

Online account aggregation and administration, transfers, bill payments, and product marketplaces are basic essentials for any banking app. Newer trends though, like conversational UX (chatbots), robo-advisors, and artificial intelligence can be much more complex to implement, which presents a challenge for small and medium institutions without a dedicated development team.

That’s where yet another fintech trend comes in: white-label versions of all these technologies that can be integrated into existing systems without the need for a drawn-out, expensive in-house process. This makes rolling out a feature-rich, user-friendly financial mobile app a lot less trouble than it once was.

Account management and transfers that just work

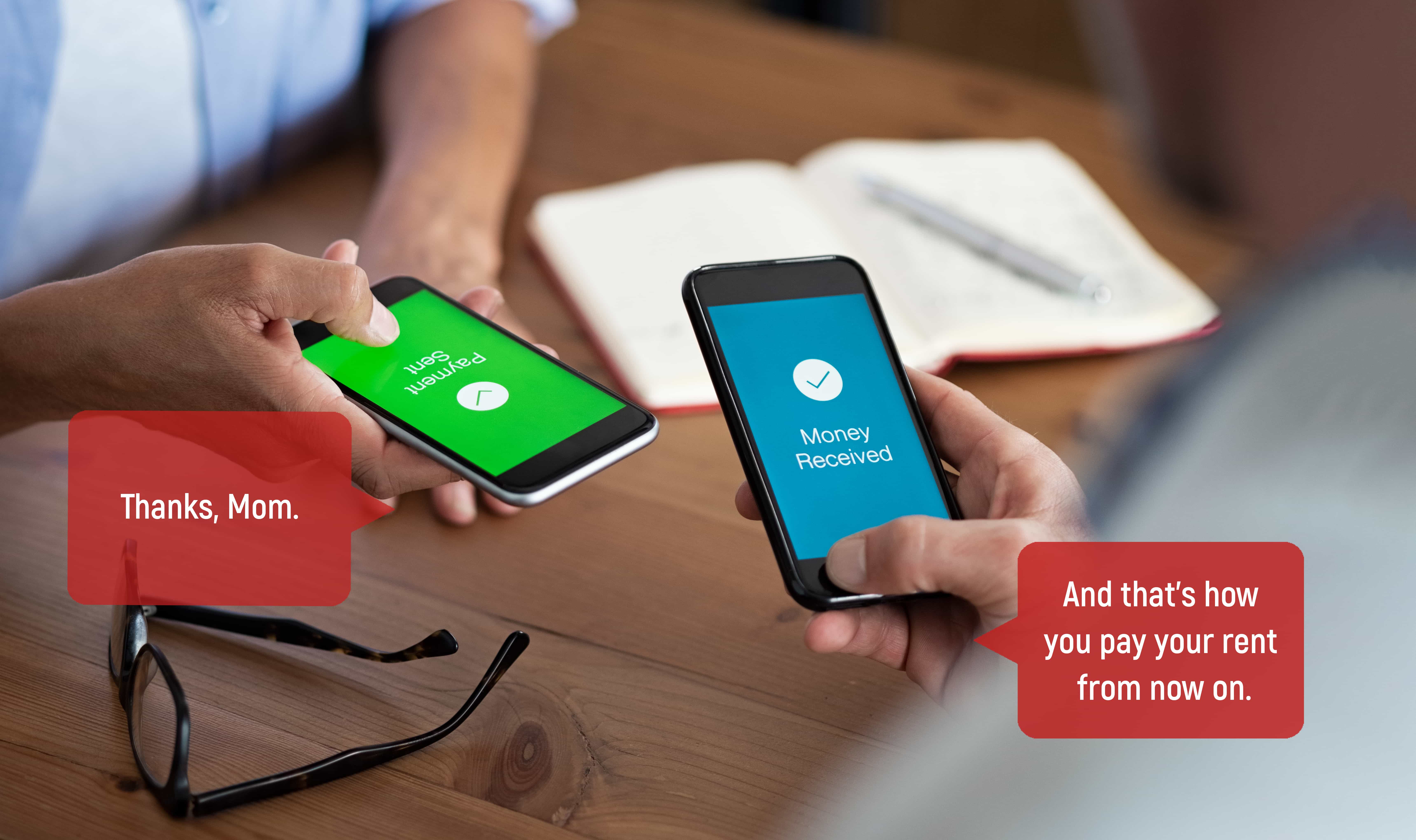

The primary goal of any financial app is to help customers keep track of their money and send it where it needs to go. Making sure these things work well should be the number one priority for any banking app. At a minimum, users need to be able to see all their account balances and transactions in a single interface, make internal and external transfers, and, optimally, pay bills and make person-to-person payments.

Having an interface that does these well is vital, but many of these basic functions can also now be accomplished via conversational UI. In many cases, this can be even quicker and easier than through conventional financial app interfaces. Being able to view a balance, send a transfer, or even pay a friend by typing a few lines into a messenger is a feature that people may grow to depend on.

An online marketplace that makes it easy to find what you need

Making a product menu available to users is a vital first step in helping users find new accounts and services, but a simple unsorted list can be overwhelming, especially to those who aren’t as financially savvy or motivated to find a new product. A good in-app marketplace should make finding products and information as frictionless and understandable as possible for every level of the user by employing an intelligent recommendation engine and an intuitive interface. Every pain point removed here is another customer group reached.

The same goes for the onboarding process. A lengthy, complex sign-up process is going to turn off less-motivated customers, so having something engaging and brief is vital. Getting a new financial product will never be as straightforward as downloading a smartphone app, but with the right treatment, it can feel just as smooth.

Conversational UI can be a big help here, as it can present suggestions and information in a simple, interactive format. It’s certainly not a complete replacement for browsing and scrolling, but it provides an engaging alternative — important to keep people from losing interest and switching away — and allows people to find answers to their questions without digging through any frustrating fine print or menus.

AI financial advisors

This is where things get a bit more complex. AI is getting more popular, but it’s still far from being a plug-and-play technology. Once the initial building and training are completed, though, an AI-powered financial assistant in an app should be able to apply machine learning algorithms to a user’s financial history, analyzing income, assets, and expenditures to provide customized advice and services.

AI’s primary use case is sorting through large volumes of data very quickly, and this means it’s exceptionally effective at presenting detailed analytics dashboards and insights to users. This goes far beyond simple monthly averages: an effective AI can identify trends in and links between income, spending, bill payments, and saving, and can provide highly individualized advice based on these.

Creating savings plans, alerting users to sudden changes in spending patterns, and providing financial coaching are just a few of the things a good AI financial advisor should be able to do. For example, after analyzing a few months of data, it could automatically figure out your regular expenses vs your irregular spending, break down both categories, and give you tips on where you might want to look for savings. It could then monitor your transactions on an ongoing bonus to assess your progress or provide alerts if something strange happens or you go off-track from your goals.

AI’s analytical capabilities fit neatly together with its natural language processing (NLP) side. Its adaptive conversational abilities allow it to efficiently answer user questions about general finance and deliver personalized insights faster than a human could and make information more directly accessible to users than web pages or FAQ sections do. This makes it a great first-line customer service tool, as well as a way for people to get a more detailed picture of their financial situation.

Robo-advisors for investments

Another AI-related tool that’s been trending recently is the robo-advisor — an automatic investment management tool that helps people build and manage investment portfolios without needing to manually buy and sell assets. Robo-advisors are, obviously, best-suited for apps with an investment focus, but their ease of use and relative cheapness have made them very popular with young investors, who are also the most likely to use mobile financial apps.

Robo-advisors typically start by creating an investment profile for each user, asking a series of questions about their current situation and end goals. They may also connect to a user’s financial accounts and analyze them to come up with investment plans and predictions that update along with the accounts. This functionality is typically related to the AI-powered financial advisors described above.

Robo-advisors are almost invariably a “set-it-and-forget-it” tool, so once an account is opened and funds are deposited, the user shouldn’t be required to do much aside from making regular deposits, with the AI doing the bulk of the day-to-day management.

New trends

Mobile apps, online marketplaces, artificial intelligence, and robo-advisors are some of the biggest trends in fintech right now, and average users are gravitating towards online platforms that provide these. Large commercial banks have already started rolling out their own chatbots, marketplaces, and AI technologies, but small and medium institutions without dedicated development teams have been having a more difficult time keeping up with the fast pace of change in the current fintech climate.

Third-party white-label solutions are becoming an increasingly popular alternative to in-house development for small-to-medium financial institutions, though, as they provide the technology without the need for costly research and development. These solutions typically just need to be integrated into a bank’s system in a one-time setup process, after which they’re ready to start working right away. Ongoing support is also generally part of the deal, minimizing the need for in-house troubleshooting or upgrades.

FINMATEX — an all-in-one solution

FINMATEX is one of the above-mentioned white-label financial apps, and it’s a highly flexible way to bring your fintech stack up to date. Its modular design allows you to mix and match components as you need: you can have an AI-powered financial advisor, chatbot, marketplace, and robo-advisor all in the same package, or you can simply select the specific functionalities that fit your use case. If you’re not in the business of managing portfolios, for example, you probably don’t need the robo-advisor, but the financial advisor and chatbot might be just the upgrade you need to upgrade your services and support.

Because it integrates directly into existing systems and brands, FINMATEX offers all the functionality and security of an in-house solution with minimal hassle and almost no third-party footprint. It integrates directly with APIs, minimizing the need for manual updating and maintenance, and can be adapted to a wide range of systems and needs.

The relative ease of setup makes the platform a cost-effective, fast solution compared to custom development, and the ongoing support services ensure the product will work smoothly and remain compliant over its lifetime. It takes a full team to keep modern banking apps humming along, and that’s what FINMATEX has behind it: the expertise and consistent delivery of a dedicated development team. Contact us to request a demo.